Automotive

Driving Change – Part 2: Media Perception

By Paige Lingwood, Insights Consultant, CARMA

The global automotive industry is undergoing a major transformation, sparked by geopolitical pressures, the rise of new Chinese competitors, supply chain vulnerabilities, and changing consumer preferences. This report analyzes online media responses to Chinese automotive brands and their impact on established global competitors throughout 2024.

Key Objectives

This analysis examines the tonality towards Chinese brands versus established brands, identifies positive and negative attributes, explores leading trends driving coverage peaks, and assesses confidence levels and skepticism in the industry’s transition.

Methodology

The study analyzed a representative sample of 12,000 articles from January 2024 to January 2025 across 15 markets including Brazil, China, France, Germany, Italy, Japan, Malaysia, Philippines, Saudi Arabia, Singapore, Spain, UAE, UK, and USA. Media outlets were selected based on automotive industry relevance, including specialist outlets, news sources, lifestyle media, and technology publications.

Industry Landscape

Chinese brands now dominate the global electric vehicle market, accounting for seven of the top 10 positions in global EV seller rankings. BYD stands out as the leading performer, with plug-in deliveries increasing 58.2% year-on-year, representing 26.1% of all EV sales in 2024. Despite this rise, established brands maintain command over global passenger car sales, with Tesla’s Model Y (1.09 million sales) and Toyota Corolla (1.08 million sales) leading 2024 sales.

Top Industry Trends for 2025

1. Tariffs Dominating Discussion

Tariffs emerged as a major issue in 2024, with the EU enforcing new import tariffs up to 45% on Chinese EVs in October. US tariffs on Chinese imports and President Trump’s reciprocal tariffs affecting over 180 countries continue driving media coverage. The “Detroit 3” (General Motors, Ford, Stellantis) face the most significant impact due to their North American operations.

2. Deeper Tech Collaboration

With Chinese brands driving rapid innovation, traditional automakers can no longer thrive independently. Notable collaborations include Toyota-Tencent, Renault-Cerence, Nissan-Baidu, Stellantis-Mistral, and Volkswagen-Horizon Robotics. These partnerships are evolving into deeper relationships, acquisitions, or mergers.

3. Autonomous Driving and Software-Defined Vehicles

By 2025, 60% of newly sold cars will feature autonomous driving capabilities like adaptive cruise control and lane-assist. Software-defined vehicles (SDVs) represent a seismic shift, with over-the-air updates and enhanced safety becoming major selling points.

4. New Audience Engagement

Brands adapt through influencer marketing and YouTube strategies, with 80% of car buyers influenced by YouTube content during their purchase process. The Consumer Electronics Show (CES) has emerged as a key automotive showcase, eclipsing traditional auto events.

5. TikTok’s Emerging Role

While TikTok accounts for just 4% of potential car buyers, brands focus on the platform for Gen Z influence. TikTok released new automotive advertising formats in February, positioning itself as a full-funnel platform for the industry.

Key Findings

Media Perception Alignment

Chinese brands receive characteristically low criticism and high positive coverage on crucial factors like pricing, technology, and reliability. This aligns with consumer research showing price, reliability, and technology as key purchase decision factors.

BYD’s Dominance

BYD leads share of voice with double the coverage volume compared to brands like Geely, Volkswagen, and BMW. The brand generates 41% of all positive Chinese brand coverage, with 37% of BYD’s coverage being positive versus 30% for Chinese brands overall and 24% for established brands.

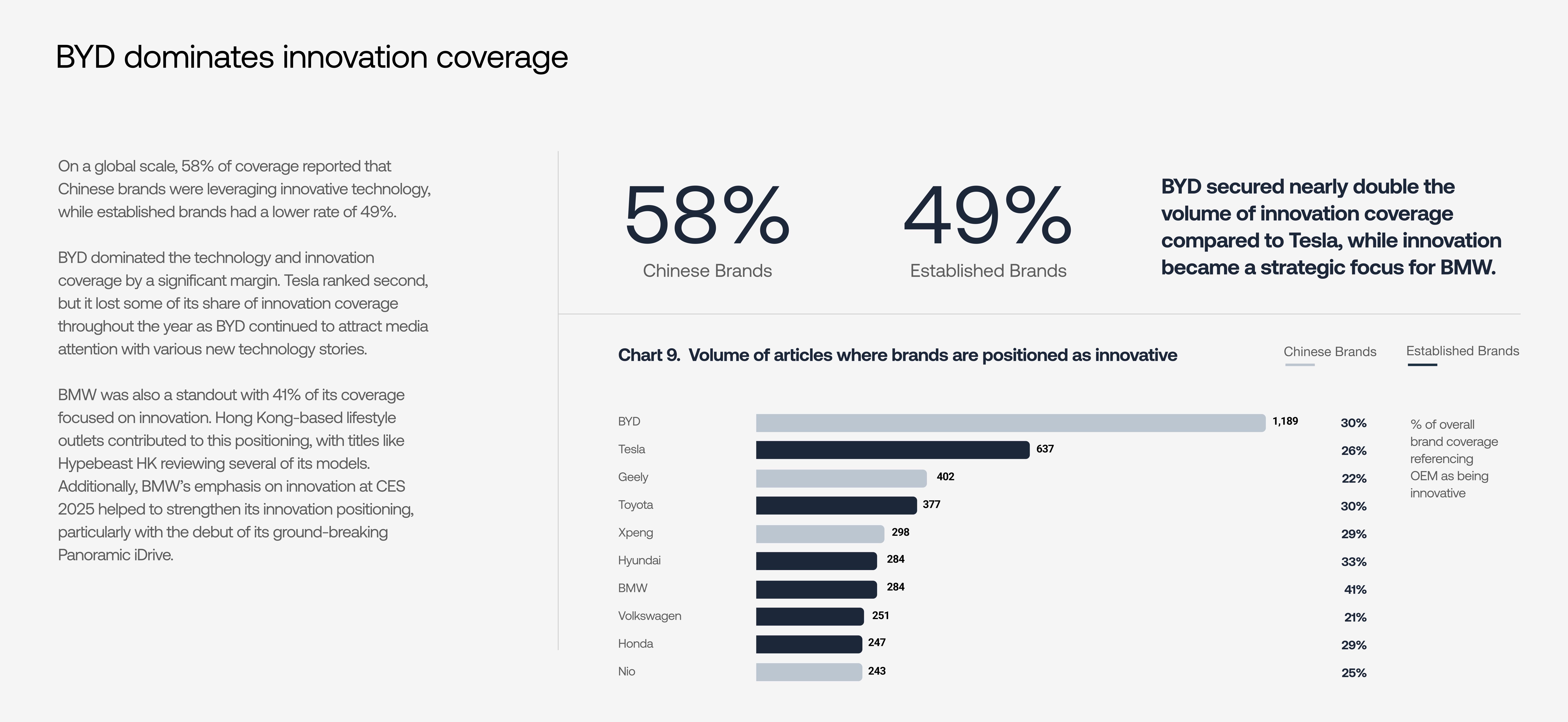

Innovation Leadership

Close to 60% of media coverage reported Chinese brands utilizing innovative technology compared to 50% for established brands. UAE-based media contributed significantly to this positive technology focus, elevating Chinese brand perception in the Middle East.

High Confidence Levels

Media express high confidence and low skepticism toward Chinese brands overall. Brands like Haval, Wuling, Zeekr, and Chery showed the highest confidence proportions, while Chrysler, Volkswagen, SAIC, and Tesla received the most skeptical coverage.

Coverage Trends Throughout 2024

The period between April and May marked a turning point as Chinese brands gained higher share of voice for the first time. This trend reversed from September when established brands captured attention with financial results and forecast cuts.

Tariff discussion peaked mid-year as the US quadrupled charges for Chinese imports, with 25% of tariff coverage occurring in July alone. Battery Electric Vehicles dominated both media coverage and global EV sales, driven by debates on tariffs and pricing wars between Tesla and BYD.

Consumer Decision Factors

Price, reliability, and technology received positive Chinese brand coverage across multiple markets. Onboard technology emerged as a clear advantage, facing minimal criticism. The US Information Technology & Innovation Foundation reported Chinese EV brands are 30% faster at developing and launching new models compared to established brands.

BYD secured nearly double the innovation coverage volume compared to Tesla, while BMW achieved 41% innovation-focused coverage. Globally, 58% of Chinese brand coverage highlighted innovative technology versus 49% for established brands.

Media Confidence Analysis

Journalists globally express confidence toward Chinese brands’ future, with limited outright skepticism. BYD alone contributes 36% of overall Chinese brand confidence, while Tesla leads established brands with 11% confidence contribution.

The Philippines displayed highest confidence in Chinese brands, particularly GAC, while UK and Saudi Arabia contributed nearly 30% of global skepticism, primarily focused on tariff expansion impacts.

Conclusion

Chinese automotive brands, led by BYD, are successfully redefining industry dynamics through positive media positioning aligned with consumer preferences. The synergy between earned media coverage and consumer decision factors indicates a winning formula in the competitive landscape. As the industry continues evolving through technological advancement, regulatory changes, and shifting consumer behavior, the ability to adapt, collaborate, and connect with audiences will determine success.

The rise of Chinese brands represents more than market disruption—it signals a fundamental transformation in how automotive companies approach innovation, technology integration, and consumer engagement in an increasingly digital and environmentally conscious marketplace.