Financial

Payments Security: The Key to Winning Consumer Loyalty in MENA

The adoption of digital commerce in MENA has skyrocketed over the past few years. Countries that were once deeply attached to cash and physical transactions have shot to digital maturity in just a few years. According to Checkout.com’s 4th annual MENA ecommerce report, The State of Digital Commerce in MENA 2024, 91% of the region’s consumers have reported shopping e-commerce in the past two years. The number of people who shop online in MENA at least once per day has grown by 80% since 2020, with the Kingdom of Saudi Arabia leading the way with a staggering 90% increase.

In response to evolving consumer demands, merchants across MENA are embarking on ambitious digitization journeys and adopting innovative payment strategies. As digital commerce moves beyond the early-adoption phase, the focus is shifting toward fine tuning performance. In doing so, strengthening payment security has become a top priority.

As innovation stimulates advancements in the payment industry, fraudsters don’t rest on laurels, further sophisticating their own scam methods and tricks. Furthermore, the very aspects of e-commerce that make it an enticing prospect for consumers – speed, convenience, and anonymity – also work in cybercriminals’ favor. Because the e-commerce ecosystem includes multiple stakeholders, the retailer, the customer, the processor, and the networks, fraudsters have multiple potential access points that they can exploit.

According to Remo Giovanni Abbondandolo, General Manager – MENA at Checkout.com, ecommerce fraud can take many forms, such as criminals using stolen credit card numbers to make purchases, transaction replays, and chargeback fraud. The diverse and complex nature of e-commerce fraud emphasizes the importance of vigilance and secure practices merchants must adopt to avoid such incidents.

But it’s not just the initial financial loss that merchants need to be concerned about. Falling prey to ecommerce fraud can damage customer trust and the company’s reputation. Alarmingly, 33% of MENA consumers say they have been a victim of payments fraud. According to The State of Digital Commerce in MENA 2024 report, safe and secure checkout is now a priority for 39% of MENA consumers. In contrast, in 2020, survey respondents placed the highest value on speedy delivery.

Furthermore, up to 30% of shoppers have said a single falsely declined payment- when a payment is declined despite the payee having sufficient funds in the account, would lead them to shop from a competitor’s website. With the cost of customer acquisition for e-commerce merchants having increased, a rise in falsely declined payments adds insult to injury. This makes high-performing acceptance solutions a matter of huge competitive importance in MENA.

To this point, it’s important to mention that the region also continues to see a relatively high number of false declined payments. According to Checkout.com’s latest report, 23% of respondents experienced a falsely declined payment in recent months. In today’s fast-paced digital economy, consumers are also less patient, less loyal, and savvier than before.

Shoppers want to know their payment is being handled by a safe and reliable partner. The good news for merchants is that fortifying payments security is a much simpler task than dealing with widespread data breaches.

In this context, Abbondandolo outlines effective strategies that merchants in MENA can adopt to minimize payment fraud and false declines, thereby enhancing consumer trust and loyalty.

- Choose a trusted partner

Partnering with a regulated payments service provider (PSP) that offers acquiring capabilities, advanced technology support, and comprehensive regional regulatory expertise can significantly bolster a business’s security measures against fraud. Regulated PSPs provide acceptance solutions that enhance payment processes through optimized messaging, routing, and retries, ensuring robust security and seamless transactions throughout. Furthermore, because fraudsters have no boundaries, partnering with a regulated global PSPs with local experience offers advanced technology solutions that include real-time fraud detection systems that are trained on detecting the most advanced global fraud scams and techniques. By analyzing transactional data in milliseconds, identifying suspicious patterns and behaviors that may indicate fraudulent activity.

By partnering with a regulated PSP that offers acquiring capabilities and advanced technology support, businesses can benefit from a holistic approach to fraud prevention and payment security.

- Harness the power of embedded AI

Regional merchants are increasingly safeguarding their businesses from fraud by leveraging a combination of tools and machine learning. Advanced payment technology empower merchants to seamlessly integrate fraud detection solutions into their platforms, without requiring additional set up. Meanwhile, AI is now trained on billions of global transactions, with merchants benefitting from a global network effect that allows them to analyze vast amounts of data to detect patterns, anomalies and emerging fraud like never before.

Minimizing fraud and improving performance in payment processing are closely intertwined goals that can significantly impact a business’s bottom line and customer satisfaction. When a business effectively reduces fraud, it tends to experience several concurrent benefits that contribute to overall performance enhancement.

Our merchants in the region have been benefiting from a whole new level of payment performance with Intelligent Acceptance. This product combines advanced Artificial Intelligence and Machine Learning, vast network data, and deep payment expertise to increase conversion and unlock untapped revenue. We have already recovered $1.1 billion of revenue, and increased acceptance rates on average by 2% for globally.

- Make data work for you

Research conducted by Checkout.com alongside Oxford Economics found that $50.7 billion was lost due to false declines in recent years. Large data sets can empower merchants to track and respond to customer payment trends with laser accuracy in real-time. Here we have seen the great benefit from Intelligent Acceptance that draws on insights from these data sets to deliver a whole new level of payment performance, increasing conversion and unlocking untapped revenue, as well as Network Tokens that have helped our merchants achieve higher authorization rates, reduced fraud and allow businesses to offer an improved customer experience, while keeping customers data

Looking ahead, half of all shoppers in MENA anticipate an increase in their online spending over the next 12 months. Abbondandolo believes that MENA merchants still have significant untapped opportunity to combat fraud, reduce false declines and their overall payments costs, while increasing their revenue. As consumers increasingly embrace digital shopping and payments, optimizing every aspect of the ecommerce experience remains crucial for merchants to capitalize on this growing trend.

As geopolitical uncertainty, tighter liquidity and digital disruption converge, the CRO role is evolving from compliance gatekeeper to strategic business leader.

For much of the past decade, GCC banks operated in an environment defined by strong liquidity, rapid credit expansion and relatively stable macroeconomic conditions. Supported by high oil revenues and ambitious national growth agendas, the region’s banking sector became synonymous with resilience, scale and sustained growth.

That resilience has been tested in recent months and, so far, the sector has responded well. Recent banking data published by the Central Bank of the UAE (CBUAE) and the Saudi Central Bank (SAMA) suggests that customer deposits have continued to grow despite heightened regional uncertainty.

Customer deposits increased by 17% year-on-year as of April 2026, and 2% from February to April 2026 in the UAE, while in Saudi Arabia, the growth in deposits was 11% year-on-year as of April 2026 and 2% from February to April 2026 , reinforcing both markets’ positions as regional safe havens for capital. Growth in monetary aggregates and non-resident deposits further suggests that regional and international investors continue to view GCC banking systems as stable, well-capitalized and resilient.

Importantly, there is little evidence so far of the capital flight or systemic liquidity pressures that some observers initially feared. Instead, the data suggests that the UAE and Saudi Arabia continue to play an important role as regional safe havens for capital, supported by strong banking fundamentals, prudent regulation and proactive central bank intervention.

Central banks have also played an important role. Proactive interventions helped preserve liquidity, support credit expansion and provide targeted relief to sectors facing short-term disruption. In the UAE, banks were able to extend working capital facilities and restructure short-term obligations for fundamentally healthy businesses, helping bridge temporary cash-flow pressures while maintaining confidence across the financial system.

As a result, resilience is no longer simply a measure of capital strength. It has become a strategic capability that underpins the sector’s ability to navigate an increasingly complex operating environment.

However, what is clearer than ever before is that the operating environment around banks is changing rapidly—and as a result, so is the role of the CRO.

The recent regional conflict accelerated that realization. Traditional stress-testing models were largely designed around financial shocks such as market volatility, liquidity tightening, and credit deterioration. What many institutions are now confronting is a far broader challenge, where geopolitical tensions, cyber threats, operational resilience, and credit risk can all influence one another simultaneously.

Across the GCC, this has prompted some banks to reassess whether existing business continuity and resilience frameworks are sufficiently equipped for a far more interconnected risk landscape.

This is particularly relevant in a region where regulatory frameworks have prioritized sovereignty, local data residency, and operational control. Recent events have also created an opportunity for institutions to reassess how these strengths can be balanced with greater operational flexibility and diversification, e.g., for digital data storage.

At the same time, a second structural shift is unfolding more quietly beneath the surface.

According to analysis from FTI Consulting, GCC banks originated close to $1 trillion in new lending between 2020 and 2025 across Saudi Arabia, the UAE and Qatar. Much of this growth took place during a prolonged low-interest rate environment and elevated liquidity conditions, meaning many portfolios, particularly across real estate and mortgage lending, have not yet been tested through a full economic stress cycle.

That could create a more complex operating backdrop for the years ahead.

For banks, the longer-term risk is not simply operational disruption. While business continuity and cybersecurity remain critical priorities, credit risk remains equally important. If short-term disruption were to evolve into a prolonged economic slowdown, pressure could emerge across borrower segments and asset classes, particularly in sectors that have benefited from strong credit expansion in recent years. In certain scenarios, a meaningful correction in real estate markets would have implications not only for borrowers but also for portfolio performance and risk provisioning across the banking sector.

This is precisely the type of forward-looking scenario that CROs must now anticipate, rather than simply respond to.

Modern CROs are increasingly expected to balance resilience, growth, operational continuity and profitability simultaneously, while helping institutions navigate a far more dynamic and interconnected operating environment. More importantly, the CRO can no longer afford to be purely backward-looking.

The institutions likely to outperform over the next decade will be those capable of identifying disruption early, adapting faster and embedding risk intelligence directly into strategic decision-making.

That requires a fundamentally different approach to risk management. One built around predictive intelligence, integrated scenario planning, dynamic stress testing and real-time decision-making.

Artificial intelligence and advanced analytics are becoming increasingly important in that transition.

Some leading regional banks are already investing in AI-enabled underwriting, early-warning systems and advanced collections capabilities that allow them to identify stress signals earlier and make more sophisticated portfolio decisions in real time. Others, however, continue to rely on fragmented legacy systems, manual workflows and reactive operating models.

That gap may become increasingly important during periods of disruption. Institutions that can identify emerging stress earlier, underwrite more effectively and anticipate portfolio deterioration before competitors will inevitably benefit from lower risk costs and stronger resilience outcomes.

Because in this new environment, resilience itself is becoming a competitive advantage.

The banks most likely to succeed will not necessarily be the largest or most conservative institutions. They will be the organizations capable of integrating risk more directly into strategic decision-making, modernizing operational infrastructure and responding dynamically to an increasingly volatile external environment.

The broader lesson for the sector is clear.

The GCC banking industry is entering a new era where resilience can no longer be measured purely through capital strength or regulatory compliance. Increasingly, resilience will be defined by adaptability and the ability to proactively anticipate interconnected geopolitical, operational, technological and economic disruption in real time.

And that shift is fundamentally redefining the CRO mandate across the region.

The institutions that recognize this early and empower their risk functions accordingly will likely be best positioned for the next phase of growth across GCC banking.

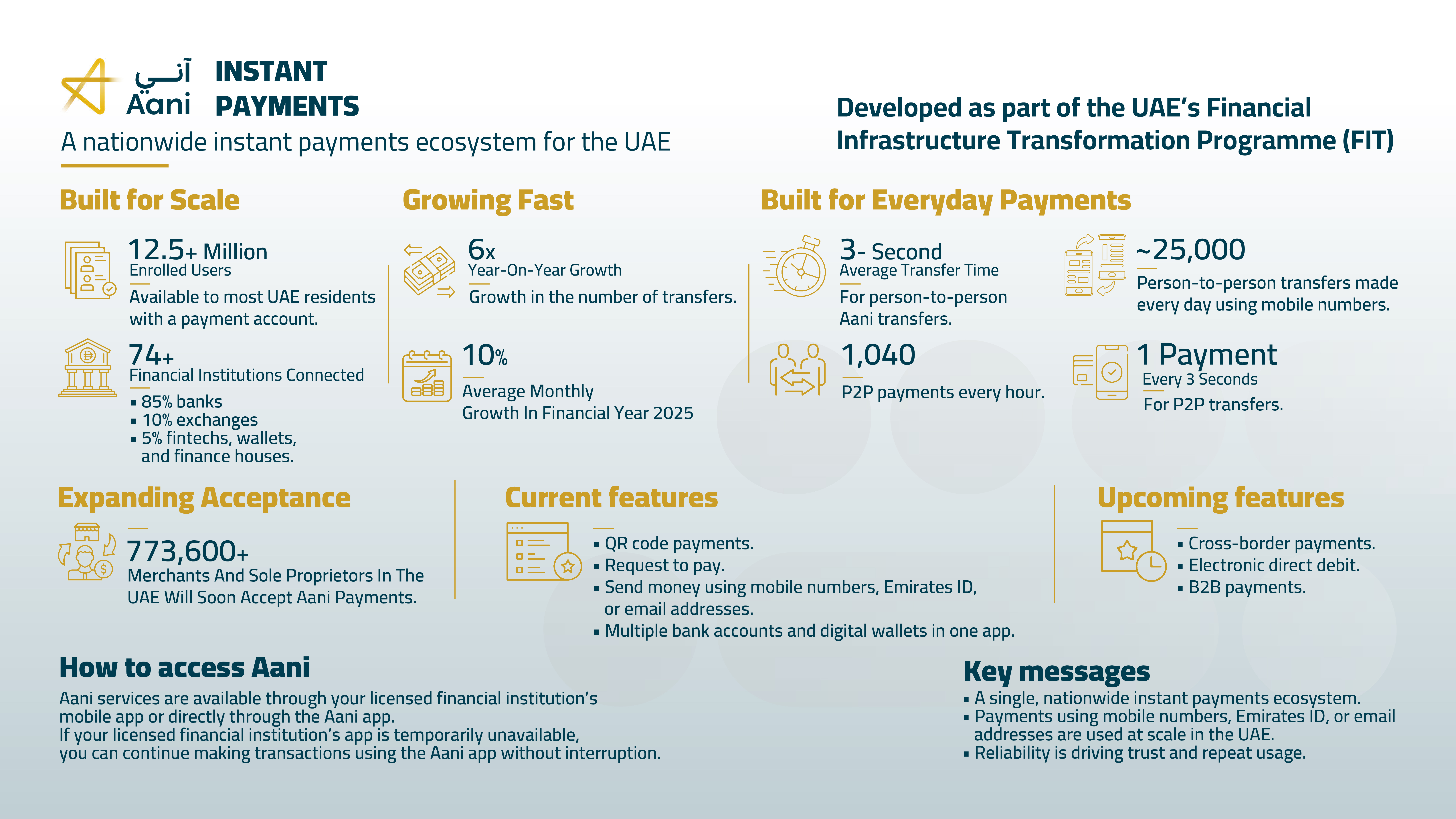

A few years ago, most conversations around instant payments focused on speed. How fast can money move? Can transfers happen instantly? Can settlement operate around the clock? Those questions mattered because many markets were still building the underlying infrastructure required for real-time payments.

The UAE entered this space differently.

Digital payments were already widely used. Contactless behaviour was established. Consumers were comfortable using banking apps and wallets for daily transactions. The starting challenge was not introducing digital payments – it was making account-to-account payments practical enough to become part of everyday behaviour.

That distinction shapes many of the decisions behind Aani.

Aani was developed as part of the UAE’s Financial Infrastructure Transformation (FIT) Programme to enable instant account-to-account payments across banks, exchange houses, fintechs, and wallets through a common national infrastructure.

Today, more than 12.5 million users and 700 thousand merchants and SMEs are enrolled on Aani, through over 74 licensed financial institutions across the country.

Those numbers show reach, but reach alone does not create habitual usage.

People do not change payment behaviour because infrastructure exists. They change behaviour when the alternative becomes easier, faster, or more reliable within everyday situations. That is where account-to-account payments become more interesting.

One of the clearest examples is proxy-based transfers using mobile numbers. Users no longer need to exchange lengthy account details to send money. In April 2026, over 25,000 transfers were executed daily, just using mobile numbers. The behaviour itself is simple, but reducing friction at that level matters. Small reductions in effort often determine whether a payment method becomes occasional or routine.

The same applies on the merchant side.

For businesses, account-to-account payments create an additional way to accept digital payments, where money can be immediately transferred to the merchant’s bank account, simply using a QR code payment or sending a request to pay to the customer. As merchant acceptance expands across the UAE, usage is gradually extending beyond person-to-person transfers into day-to-day commercial activity.

Most merchants and sole proprietors across the UAE are expected to accept Aani payments.

This shift is still developing, but it reflects a broader movement toward payment experiences that are immediate, simpler to initiate, and more closely connected to existing banking relationships.

Scale also depends heavily on ease of usage and reliability.

Consumers rarely adopt new payment behaviour because a standalone application exists. Usage grows when payment capabilities are integrated into tools people already use regularly. Aani services are available through mobile apps provided by their participating financial institutions, as well as through the Aani application itself, which means users can access instant payments within their existing banking apps rather than learning entirely new payment flows.

Achieving that familiarity required to reduce behavioural resistance is a key target that we keep in mind when developing any new product feature. Building a national payment capability is not only a technical exercise. It requires coordination across customer experience, operational readiness, dispute handling, fraud controls, onboarding journeys, and merchant acceptance. These are just some of the aspects that contribute to enhance the user experience and repeated usage of the payment scheme.

Another critical item is to ensure user experience consistency, across the various players in the ecosystem: while the infrastructure may be centralised, the customer experience is distributed across many institutions and channels.

That coordination becomes more important as payment use cases expand.

Current Aani services include proxy-based transfers, QR payments, Request to Pay functionality, and the ability to access payments from multiple bank accounts and wallets within a single application. The next phase will cover electronic direct debit, cross-border payments, e-cheques, and business-to-business transactions – additions that expand the types of financial activity moving through real-time infrastructure rather than simply adding features.

Current and upcoming functionalities will shape different expectations of the financial institutions and their end customers, being individuals or corporates, who are part of the ecosystem.

They will not just expect round the clock availability of services and speed, but also ease of usage, convenience, seamless experience, low cost of transactions and

The harder measure of success is not whether transfers can happen in seconds. The infrastructure already allows that. The more difficult task is becoming efficient and seamless enough that the behaviour repeats without conscious effort. That is usually when payment systems become part of daily life rather than simply another available option.

Last year, while the financial press was busy writing obituaries for crypto and Bitcoin was sliding off front pages, something genuinely significant happened in global payments. Stablecoins processed $33 trillion in transactions, more than Visa and Mastercard combined, which together handled $25.5 trillion. That is not a rounding error. That is a structural shift in how money moves around the world, and it happened with almost no mainstream commentary.

By Raj Kamal

I have spent the better part of two decades in payments. I have watched the industry move from cash to card, from card to mobile wallets, from domestic rails to real-time systems. And I can say with some confidence that what happened quietly in 2025 belongs in the same conversation as those transitions. The difference is that this one was mostly invisible to the people who usually lead that conversation.

The Numbers Deserve Context

Before we get too far, there is a legitimate caveat worth addressing upfront. Not all of that $33 trillion represents the kind of payment activity you might imagine, a supplier invoice settled in Dubai, a remittance sent from a worker in Sharjah to a family in Karachi. A McKinsey and Artemis Analytics report from early 2026 stripped out trading activity, DeFi cycling, and internal fund shuffling and found roughly $390 billion in what they called “genuine end-user payments.” That figure, they noted, more than doubled from 2024.

So the honest version of the story is this: even on the most conservative read, genuine stablecoin payment activity doubled in a single year. And on the broader rails measure, stablecoins have now outscaled the world’s two largest card networks. Both of those things are true simultaneously. The volume growth is also not speculative froth. It is coming from businesses.

B2B transactions now account for roughly 60% of all genuine stablecoin payment volume. Monthly B2B flows surged from under $100 million in early 2023 to over $6 billion by mid-2025, a 60x increase in 30 months.

An EY-Parthenon survey of 350 corporate and financial institution executives found that 62% of current stablecoin users are using them specifically to pay suppliers. Ship brokers. Steel traders. Import-export businesses. These are treasury teams who found a faster, cheaper way to move money across borders and adopted it without waiting for permission from the mainstream financial narrative.

Why It Happened Quietly

Part of the answer is timing. The growth of stablecoin payment infrastructure coincided almost perfectly with a period of intense negative sentiment around cryptocurrency broadly. Bitcoin volatility, exchange collapses, regulatory battles in the United States, all of it generated enormous noise. Underneath that noise, a parallel financial infrastructure was being quietly assembled.

The other part of the answer is that stablecoins solved problems that the payments industry had been struggling with for years. Cross-border payments through correspondent banking networks are slow, opaque, and expensive. A typical international B2B transfer can take two to three days and lose 3-6% to fees and foreign exchange costs. Stablecoins settle in seconds, operate 24/7, and carry transaction costs that are a fraction of the traditional alternative. When you frame it that way, the adoption curve makes complete sense.

The incumbents noticed. Stripe acquired stablecoin infrastructure provider Bridge for $1.1 billion and launched stablecoin payment acceptance across more than 100 countries. Mastercard acquired BVNK, a stablecoin infrastructure firm, in March 2026. Visa settled $4.5 billion annually in stablecoins as of January 2026 and is integrating USDC into its core settlement operations. These companies are not making billion-dollar bets on a trend they expect to reverse.

The UAE Is Not Playing Catch-Up

This is where it gets specifically relevant for this region, and where I would push back on anyone who assumes the Middle East is watching from a distance.

The UAE has spent the last two years building regulated stablecoin infrastructure with a seriousness that few jurisdictions globally can match. The Central Bank of the UAE issued its Payment Token Services Regulation in mid-2024, establishing a comprehensive framework requiring 100% reserve backing for payment tokens and creating clear licensing pathways. This is not a sandbox experiment. It is a formal financial regulatory structure.

In October 2024, AE Coin became the first fully licensed AED-pegged stablecoin, issued through a partnership with Al Maryah Community Bank. In January 2026, the CBUAE registered USDU, the country’s first USD-backed stablecoin, with reserves held onshore at Emirates NBD, Mashreq, and Mbank. In December 2025, ADNOC Distribution signed an agreement to accept AE Coin across nearly 980 service stations across the UAE, Saudi Arabia, and Egypt. That is one of the largest retail deployments of a regulated payment token anywhere in the world.

At the same time, the UAE’s domestic payment systems processed more than AED 20 trillion in transfers in just the first ten months of 2025. The country is consistently among the world’s largest sources of outbound remittances, with a workforce that sends money to families across South Asia, Southeast Asia, and East Africa every month. The friction in that system is exactly what stablecoin rails are designed to remove.

The UAE ranked third globally in digital asset transaction volume at $34 billion for the year ending June 2025. That ranking reflects genuine activity, not speculative positioning.

What Payments Veterans Should Take From This

I am not suggesting that traditional payment rails are disappearing. Visa and Mastercard are actively integrating stablecoins rather than being displaced by them, which is itself a significant signal about where the industry is heading. The more important observation is about infrastructure decisions being made right now, in this decade, that will determine which payment corridors are competitive in the next one.

The UAE’s approach, regulated frameworks, onshore reserve requirements, licensed issuers, interoperability with the Digital Dirham, is a serious attempt to capture a structural moment rather than react to it. Stablecoin transactions by value are projected to exceed $50 trillion in transaction volume in 2026 alone. Five to ten percent of cross-border payments globally are expected to run on stablecoin rails by the end of the decade.

For anyone building in payments, moving money across borders, or managing treasury in this region, the relevant question is no longer whether stablecoin infrastructure matters. The relevant question is whether your organisation is positioned on the right side of the infrastructure that is being built.

The shift happened while people were arguing about whether crypto was real.

About the Author:

Raj Kamal is Founder and CEO of TransFi, a cross-border payments and stablecoin settlement infrastructure company that has processed over $1 billion in payment volume across Asia, MENA, Africa, and Latin America.

THE REALITY OF AI DEPLOYMENT ACROSS THE WORKFORCE IN THE REGION

CELEBRATING WORLD CHOCOLATE DAY WITH A HEALTHIER CHOCOLATE SNACK

BELKIN UNVEILS ON-THE-GO COLLECTION TO KEEP TRAVELLERS POWERED UP THIS SUMMER

-

News11 years ago

SENDQUICK (TALARIAX) INTRODUCES SQOOPE – THE BREAKTHROUGH IN MOBILE MESSAGING

-

Trending8 months ago

Trending8 months agoOPPO A6 Pro 5G Review: Reliable Daily Driver

-

Tech News2 years ago

Tech News2 years agoDenodo Bolsters Executive Team by Hiring Christophe Culine as its Chief Revenue Officer

-

VAR1 year ago

VAR1 year agoMicrosoft Launches New Surface Copilot+ PCs for Business

-

Automotive2 years ago

Automotive2 years agoAGMC Launches the RIDDARA RD6 High Performance Fully Electric 4×4 Pickup

-

Tech Interviews2 years ago

Navigating the Cybersecurity Landscape in Hybrid Work Environments

-

Tech News12 months ago

Tech News12 months agoNothing Launches flagship Nothing Phone (3) and Headphone (1) in theme with the Iconic Museum of the Future in Dubai

-

VAR2 years ago

VAR2 years agoSamsung Galaxy Z Fold6 vs Google Pixel 9 Pro Fold: Clash Of The Folding Phenoms